The weekend ran hot. Strikes on one side, retaliation on the other, and by Sunday night a wire-service consensus that landed harder than the headlines: Washington and Tehran have agreed to resume talks, with Doha proposed as the venue and the Strait of Hormuz the central file. Multiple outlets report a start as early as Tuesday.

That is the kind of news that moves a prediction market, and Polymarket has a contract built precisely for it. The next round of US-Iran peace talks market on Polymarket asks a narrow, testable question: by which date does the next formal senior-level, in-person round actually begin? The earliest rung, June 26, has already resolved No. The decision points now sit later in the calendar.

What the contract is actually measuring

Resolution here is mechanical, not vibes. A qualifying round must be a deliberate in-person diplomatic session between US and Iranian representatives, beginning by the listed date at 11:59 PM ET. Talks scheduled, briefed about, or leaked do not count. The handshakes have to happen in a room.

That matters because the news flow and the market measure different things. The reporting points to an agreement to resume, with a proposed Doha venue and a Tuesday-ish start. The contract waits for the meeting itself to convene. A delay of even a few days, a venue swap, a last-minute Iranian recall, any of it can push the qualifying event from one rung of the ladder to the next without altering the underlying diplomatic story at all. The market is essentially a logistics tracker dressed up as a geopolitics trade.

This is one of the more useful things prediction markets do, and it is worth being honest about the shape of it. The contract is not pricing whether peace breaks out. It is pricing the boring middle layer: do the principals get on the plane, and when. Readers who want a primer on how that translates into the YES and NO sides can see our explainer on how implied probability turns into prices.

How the ladder reads after Doha

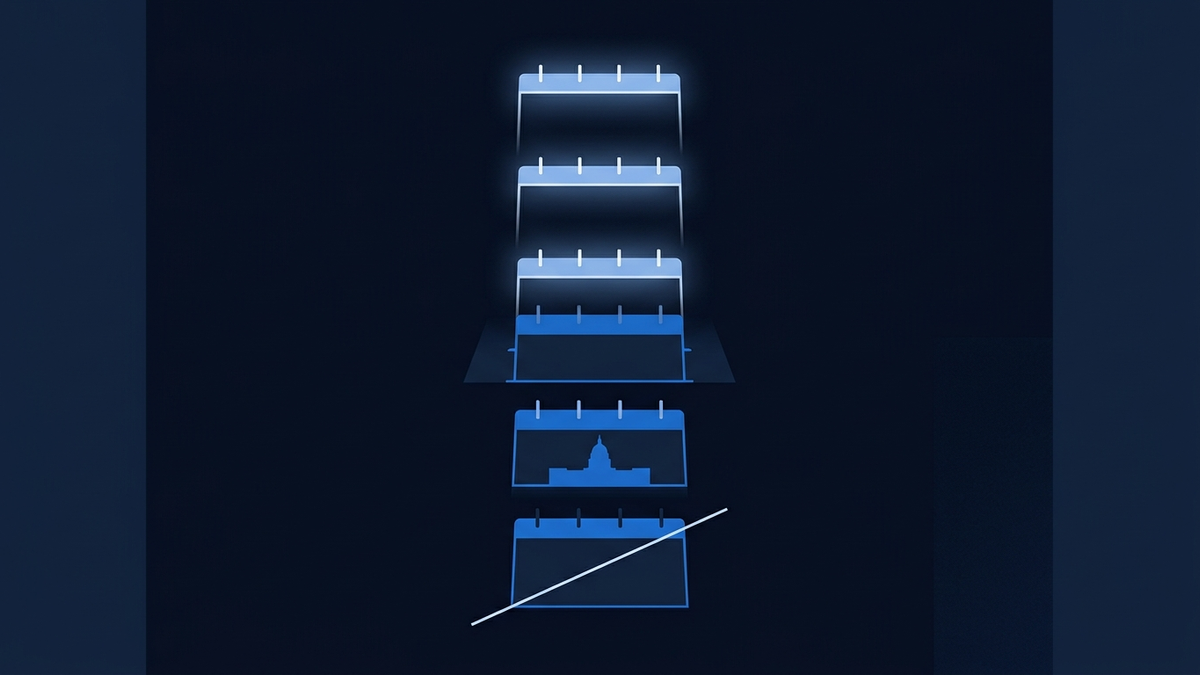

The contract has five named dates. June 26 is gone, resolved No. The remaining rungs are July 3 at 15%, July 10 at 34%, July 17 at 48%, and July 31 at 66%, all as of 29 June. The ladder is cumulative by construction: the further out the date, the more calendar there is for a qualifying meeting to land, and the higher the implied probability climbs.

The shape is consistent with what you would expect after a credible resumption signal. July 31's 66% sits clearly ahead, July 17's 48% is the contested middle, and July 3's 15% reflects the simple reality that a Tuesday meeting in Doha, even if it does happen, has to be the right KIND of meeting (senior-level, in-person, deliberate) to qualify. Lower-level technical talks or a working-group session would not trip the contract.

The July 10 and July 17 rungs both moved noticeably in the 24 hours covered by the snapshot. That is the news being priced in. Whether traders are right about the timing is a different question from whether they have correctly identified that the news matters, and the second is easier to be confident about than the first. For the mechanics of how a ladder like this is built and how the rungs relate to each other, our guide to how prediction market odds work walks through the structure.

What the Strait of Hormuz file changes

The substance of the proposed talks is, per the reporting, the Strait of Hormuz. That is a meaningful detail. Hormuz is the choke point through which a large share of seaborne crude moves, and a US-Iran conversation that takes shipping safety as its central agenda is a different kind of conversation from a nuclear-file negotiation. It is narrower, more technical, and arguably easier to convene precisely because the topic is constrained.

A tighter agenda tends to favour earlier meetings. There is less interagency choreography to do, fewer red lines to pre-negotiate, and a clearer reason for both sides to show up. None of that is bankable, and the market is right to keep meaningful probability on later dates, because diplomatic calendars slip routinely and the post-strike atmosphere does not vanish in 48 hours. But it does explain why the middle rungs look priced for genuine contest rather than settled lean.

Volume on the contract has run into the low six figures over the past day, up sharply on the news. That is still thin by Polymarket standards, which is itself a useful signal: this is a logistics market for people who follow the file closely, not a viral political contract. Thin books move fast on real news, and the rung-by-rung shifts reflect that.

The honest read

The news is real and the market has registered it. Doha is on the table, the agenda is Hormuz-shaped, and the calendar question has narrowed to four live dates. What the contract cannot tell you is whether the talks, once convened, achieve anything. Resolution closes the moment people sit down. Everything that matters substantively, the de-escalation, the shipping protocols, the durability of any understanding, plays out afterwards and on other markets entirely.

iPredicta tracks the US-Iran ladder alongside the broader cluster of Middle East contracts on Polymarket and the regulated venues, because the value of these markets right now is exactly this kind of calendar-anchored reading: did the meeting happen, by when, and what does the price say about how seriously traders take the resumption signal.

Frequently asked questions

What counts as a qualifying round of talks for this market?

The contract resolves Yes if the next formal senior-level round of US-Iran peace talks begins in person by the listed date at 11:59 PM ET. It has to be a deliberate diplomatic session between representatives of both governments. Lower-level technical sessions, phone calls, or proxy conversations do not qualify.

Why has the June 26 rung already resolved No?

The earliest date on the ladder passed without a qualifying senior-level in-person meeting taking place, so that leg settled No and is now eliminated. The live decision is now spread across the four remaining rungs from July 3 through July 31, with July 31 carrying the highest implied probability as of 29 June.