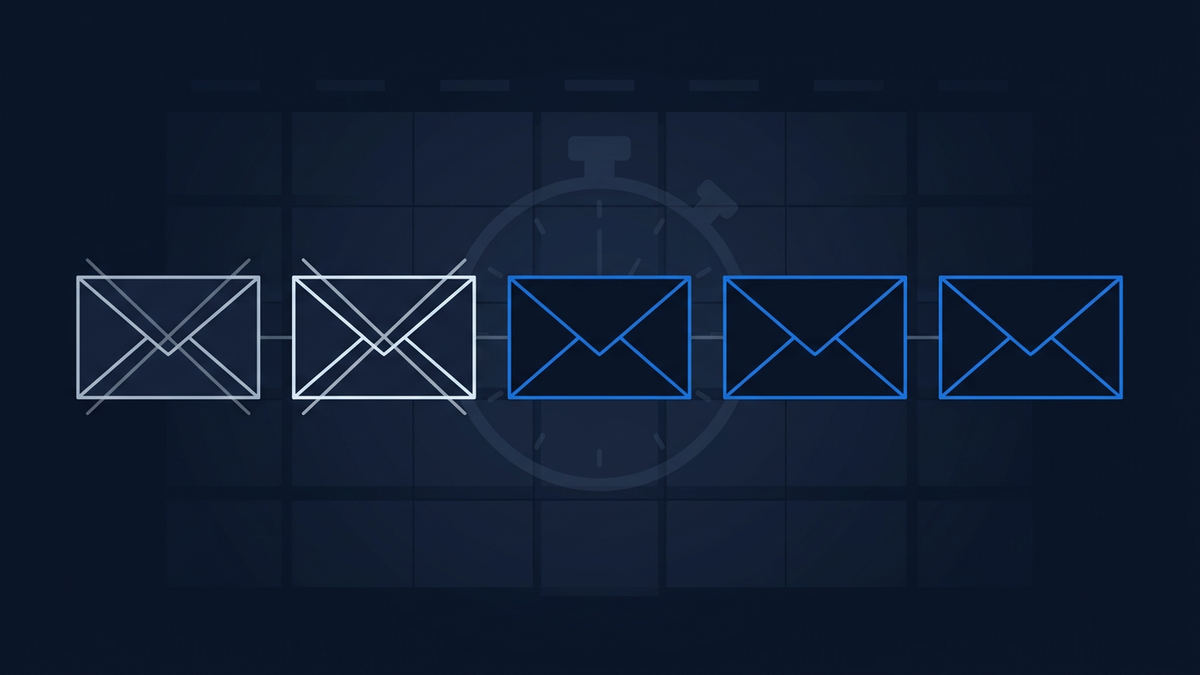

Two of the five dates have already come and gone with nothing to show for them. That is the quiet headline on Polymarket's Ventuals token launch market, where the questions about a December 2025 launch and a March 2026 launch have both resolved No. No actively transferable token appeared by either deadline. Those legs are settled fact now, not live odds.

What is left is a stack of three remaining dates and a market that is steadily working through its own calendar. The June 30 2026 question is priced under a percent as of 21 June 2026, with the September 30 and December 31 legs each trading around 5%. The contract has not been answered Yes by anyone yet. Whether it ever will is the standing question.

A simple Yes/No, asked five times

The resolution rule is unusually clean. Each leg asks whether Ventuals, the project at the @ventuals handle, has officially launched a governance token by 11:59pm ET on the date in the title. The token has to be actively and publicly transferable and tradable. An announcement does not count. A testnet does not count. A wrapped placeholder does not count. The bar is a real, live, tradable token, and Polymarket will lean on Ventuals' own communications plus a consensus of credible reporting to decide.

That clarity is worth dwelling on. A lot of crypto launch markets get tangled in definitional knife-fights about what counts as "live" or what counts as "the" token. This one mostly does not. Either the token is trading by the deadline or it is not. The resolution mechanics that decide a prediction market sometimes leave room for argument; here the rule is concrete enough that the two expired legs were settled without controversy.

The other thing the structure tells you is that this is not a question about a single date. It is the same question asked at five different points in time. Once a deadline passes without a token, that specific question resolves No and the next deadline takes over. The market is, in effect, a deadline-by-deadline diary.

What the resolved legs already tell us

The December 31 2025 leg closed without a token. The March 31 2026 leg also closed without a token. Both are eliminated outcomes now, decided facts on Polymarket's books. Anyone who held No on either has been paid; anyone who held Yes has not. The reader does not need to forecast those two; they are over.

What the reader does need to notice is what the absence of a launch through two consecutive deadlines implies, and what has happened since. In mid-June 2026 Ventuals announced it was winding down, freezing and settling its flagship OpenAI and Anthropic perpetual markets and folding its team into another Hyperliquid project, according to its own posts and reporting from CoinDesk and others. A project that is closing its core markets is not a project on the cusp of a token launch. That is the information the remaining legs are now pricing, which is part of why they trade in the low single digits rather than higher.

Earlier in the contract's life, the remaining prices could not tell you the reason a token had not appeared: a project might be slow-walking a launch for regulatory reasons, reworking tokenomics, or waiting on a listing window. The wind-down narrows that ambiguity. The market still does not adjudicate motive, but a project that is settling its markets and dispersing its team supplies the most parsimonious read of why the later legs sit where they do.

Why the structure matters more than any single price

A standalone snapshot of "5% by year-end" is, by itself, not very useful. The number will move. Tokens get announced suddenly; deadlines tick past in silence. What is durable about this contract is the shape: a sequence of binary Yes/No checkpoints, each one resolving cleanly as its date arrives, and the next picking up the question.

That shape is part of what makes pre-token launch markets interesting for readers trying to understand a project's trajectory without staking on a token that does not yet exist. The market does the discipline for you. It forces the question into specific, dated chunks. If you want to read these prices properly, the basics of how implied probability translates a market price into a forecast are worth a quick refresher; the level matters less than its movement against the calendar.

The risk in the other direction is also worth flagging. Prediction-market launch contracts on smaller projects can be thinly traded, and as covered in our explainer on liquidity in prediction markets, thin liquidity can mean prices respond more to single trades than to genuine information. Treat the snapshots gently. Treat the resolved legs as fact.

The editorial take

The interesting thing about the Ventuals contract is not whether 5% is the right number on either of the remaining 2026 legs. It is that two of its five questions have already answered themselves, and the project is now reportedly winding down its operations rather than building toward a launch. Every deadline that passes without a token compresses the remaining ones, and a closing project compresses them further. That is the structural point worth holding onto: the diary has most likely become a record of a launch that will not come.

iPredicta tracks crypto launch contracts like this one across Polymarket and Kalshi precisely because the diary structure makes them readable. A token either arrives by the date or it does not, and the next date inherits the question. No spin, no narrative drift, just a sequence of plain checkpoints walking forward in time.

Frequently asked questions

What counts as an official Ventuals token launch under this market?

Polymarket's rule requires an actively and publicly transferable and tradable governance token, live by 11:59pm ET on the date in the title. An announcement on its own does not qualify, and neither does a closed or non-transferable instrument. The resolution leans on Ventuals' own communications plus a consensus of credible reporting.

What happens to the legs that have already resolved No?

Those questions are settled. The December 31 2025 and March 31 2026 legs both closed without a qualifying token, so anyone holding No was paid out at resolution and the Yes side received nothing. The remaining active legs ask the same Yes/No question against later deadlines, and they will resolve in the same way as each date passes.