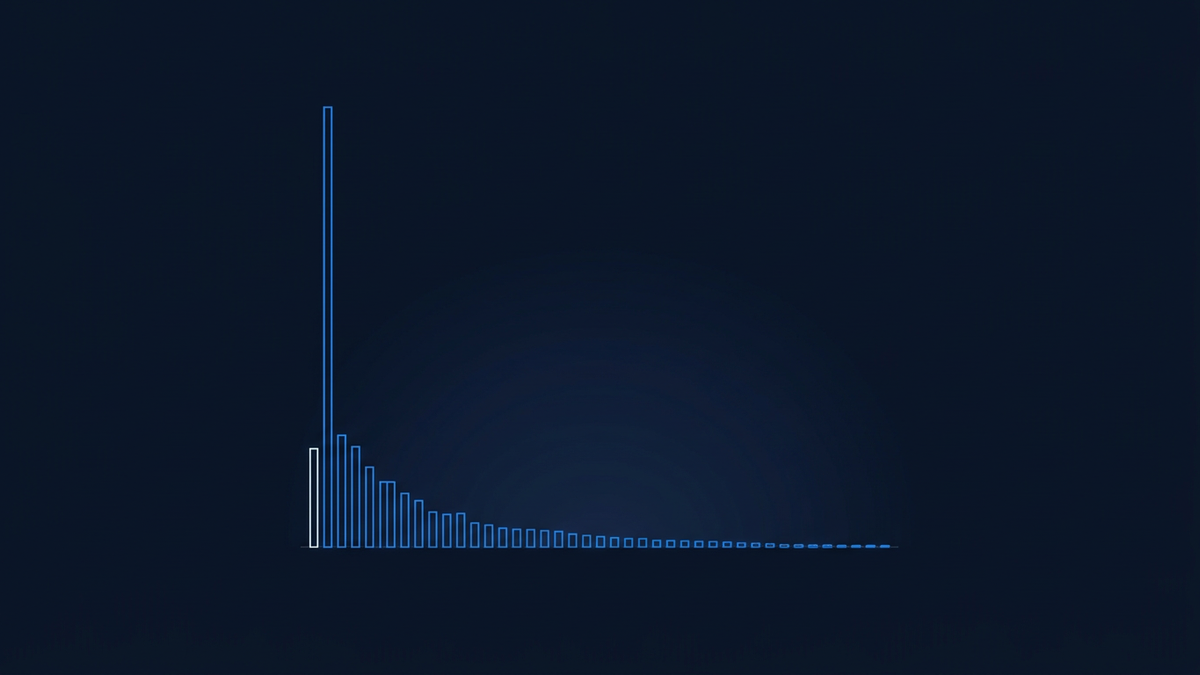

One percent of profitable users on Polymarket have captured 76.5% of all the gains. The top tenth of one percent captured 51.2%. About 69% of the roughly 2.4 million users in the dataset ended with a loss. Those are the headline figures from "Who Wins and Who Loses in Prediction Markets? Evidence from Polymarket", a 2026 working paper by Pat Akey, Vincent Gregoire, Nicolas Harvie and Charles Martineau, published as SSRN 6443103 with a public dataset hosted on Hugging Face. The paper analyses roughly $67 billion of trading. It is the first serious look at the user-level economics of a major prediction market, and the picture it draws is uncomfortable.

The question worth asking is structural. What separates the tiny group capturing most of the money from the losing majority? The researchers spend the paper answering it, and the answer is not what most casual participants assume.

It is not mostly about being right

The instinctive read is that winners forecast better. They watch the news more closely, they understand the underlying event, they call elections and sports outcomes more accurately than the crowd. The paper finds something narrower, and stranger.

On aggregate, Polymarket is well calibrated. Contracts priced at p resolve in their favour about p percent of the time. That is the property that makes prediction market prices a useful read on probability in the first place. If the average trader were systematically wrong about outcomes, prices would not behave this way.

So where does the lopsided wealth transfer come from? The researchers find it comes from execution. Winners systematically buy mispriced contracts during the brief windows when the price is wrong. Losers buy after the price has already moved. The forecasting edge exists, but it is small and modestly persistent. The dollar edge comes from how, and when, the trade gets placed.

Makers earn the spread, takers pay it

Every prediction market has two ways to enter a position. A limit order sits in the book at a price you choose, waiting for someone to come to you; you earn the spread when filled. A market order takes the best available price right now; you pay the spread. The paper finds this distinction does most of the work.

Winners are makers. Losers are takers. The top 0.1% of users supply about 47.3% of all maker volume on the platform. The bottom 95% supply about 17.1%. The concentrated winners are not predominantly informed traders calling outcomes; they are predominantly liquidity providers earning a structural fee on every trade the impatient majority makes.

The magnitude is striking. The paper finds that removing even the minimum-tick spread cost, the smallest possible execution friction, would move about 18.5% of all losing users into non-negative profit. One in five losers loses money purely on execution. Their picks are not wrong; their order type is.

This is the same shape that shows up in retail options data and in sports-betting research. The losing majority is paying a small toll on every trade, the small toll compounds, and a handful of patient counterparties collect it. The mechanic is well documented; the paper just measures it for prediction markets specifically.

A small group of skilled traders, mostly in markets they know

About 29% of traders in the dataset are classified as skilled by the paper's tests. That is not the top 29% by profit; it is the share whose performance is statistically distinguishable from luck. Even within that group, persistence is only modest. A trader who did well last quarter is more likely than chance to do well next quarter, but not dramatically so.

The more interesting finding sits inside the top 100. Of those 100 most successful users, 42 concentrate their gains in a small number of markets where they appear to have domain or event-specific expertise. The researchers look closely and conclude they look like informed traders, not insiders. They know more about a niche than the crowd, they trade that niche heavily, and they leave the rest of the market alone.

The takeaway is not that domain knowledge guarantees profit. The takeaway is that the rare profitable forecasting edge tends to be narrow. The top performers are not generalists picking everything correctly; they are specialists who picked their spots.

Many of those top performers also stop within a few months. Stopping is common across the dataset, including at the top of the distribution, which complicates any clean story about a permanent class of professional winners.

What loses money, plainly

Pull the findings together and the losing pattern is mostly mechanical. Three habits do most of the damage.

The first is paying the spread on every entry. A reader who only ever uses market orders is volunteering the structural fee that winners collect. The fix is operational, not analytical: place limit orders, wait, accept that some never fill.

The second is reacting to news after it has moved the price. By the time a headline reaches a casual participant, the market has usually already digested it. The contract is no longer mispriced; the entry is now expensive. This is the execution-timing finding restated. When you look matters more than what you think.

The third is trading without structural context. A contract at 65% is not a tip; it is a probability, and whether it is a good buy depends on what you know about the resolution mechanism, the liquidity behind the quote, and what has already happened to that price today. A reader reading the implied probability without the context around it is the type the paper finds losing money.

What helps, honestly

The research points at specific failure modes, so the responses worth talking about are the ones that map to those failure modes. Three are worth flagging, with their actual status stated plainly.

If execution timing dominates dollar outcomes, the moment a reader notices a market matters more than their view of the underlying event. iPredicta has alerts in development, with a waitlist open, designed to let users set their own thresholds: tell me when a contract crosses 75%, or moves more than 10 points in a day. That is the planned response to the timing finding. It is on the roadmap, not yet live, and it will not turn an unprofitable trader into a profitable one. It is intended to reduce the chance a reader sees a move only after it has finished.

If the bigger structural cost is paying the spread, no third-party tool can change the venue's tick. What it can do is supply enough context to judge whether a move is information or noise, and whether a market-order entry now is sensible or expensive. iPredicta's live insights layer is the response there. The analysis on the insights feed walks through specific market moves with the numbers attached, so a reader can see the shape of a move before they engage with it.

If the rare profitable edge tends to be narrow domain knowledge, most readers will never have it on most markets. The honest substitute is editorial intelligence on the markets they do not naturally follow. The live insights feed and the learn library on how prediction markets resolve are doing that work today. There is no chatbot. There is a written editorial layer staffed by people, which is a slower and narrower tool than a bot would be, and more honest about what it can and cannot tell you.

The honest backstop

None of this turns the distribution upside down. With only about 29% of traders showing measurable skill and that skill only modestly persistent, most readers will not become winning traders on these markets even with the best information and the most patient execution. That is what the paper actually documents, and any tool that suggests otherwise is overpromising.

Worth saying plainly. The value of a careful reading of prediction markets is being more informed about the world, not making money from it. The losing 69% is the base rate. A reader who treats prediction markets as a get-rich vehicle is reading them wrong, regardless of which platform they use or which feed they read.

iPredicta exists because the Akey, Gregoire, Harvie and Martineau paper documents a structure stacked against casual participants, and a careful reader benefits from seeing that structure clearly. The live editorial layer and the Top Picks market scoring are tools for reading these markets more carefully. The alerts on the waitlist are a planned response to the execution-timing finding. None of these tools produces winning trades, and the platform is honest about that. iPredicta helps you decide for yourself whether and how to engage; the rest is the market.

Frequently asked questions

What is the main finding of the Akey, Gregoire, Harvie and Martineau paper?

That gains on Polymarket are extremely concentrated and the concentration is driven by execution, not forecasting. The 2026 working paper, SSRN 6443103, analyses about $67 billion of trading across roughly 2.4 million users and finds the top 1% of profitable users capture 76.5% of gains, the top 0.1% capture 51.2%, and about 69% of all users end with a loss. The headline mechanism is that winners place limit orders and earn the spread, while losers place market orders and pay it. On aggregate the market is well calibrated, so the wealth transfer happens through execution rather than through one side being systematically wrong about the world.

Why do most prediction market users lose money?

Mostly because of small, repeated execution costs, not because their forecasts are bad. The paper finds that removing even the minimum-tick spread cost would move about 18.5% of losing users into non-negative profit; one in five losers loses purely on execution. The bottom 95% of users supply only about 17.1% of maker volume; they are predominantly takers, paying the spread on every entry. They also tend to react to news after it has already moved the price, which converts a potentially mispriced contract into an expensive one. The picks are often not wrong. The order type, the timing, and the lack of structural context are.

Are the winners on prediction markets just insiders?

The paper does not find that. Of the top 100 most successful users, 42 concentrate their gains in a small number of markets where they have domain or event-specific expertise, and the researchers conclude they look like informed traders rather than insiders. The rest of the top performers look more like patient liquidity providers earning the spread across many markets. The top 0.1% supply about 47.3% of all maker volume on the platform, against about 17.1% for the bottom 95%. The dominant winning mode is structural, not conspiratorial: showing up as a maker in size, waiting, and being selective about which markets to specialise in.

Does this mean I should not use prediction markets?

Not necessarily, but you should be honest about the base rate. About 69% of users in the dataset ended with a loss, and only about 29% of traders are classified as skilled by the paper's tests, with performance only modestly persistent. The value of careful engagement is being better informed about the world, not generating profit. If you do engage, the research points to a few sensible disciplines: use limit orders rather than market orders where you can, treat news that has already moved a price as old information, and stick to markets you actually understand. None of that overturns the distribution.

How does iPredicta fit into what the research describes?

iPredicta is a discovery and editorial platform for prediction markets, not a trading account or an advisor. The live insights feed and the learn library are the editorial-intelligence layer the research implicitly points to: structural context on markets a reader does not naturally follow, so they can judge whether a quote is finished moving or just starting. Top Picks scores markets on liquidity and uncertainty. Alerts, designed around user-set thresholds and price moves, are in development with a waitlist open and are not yet live. None of this produces winning trades. It is intended to make a reader more informed before they decide whether to engage.