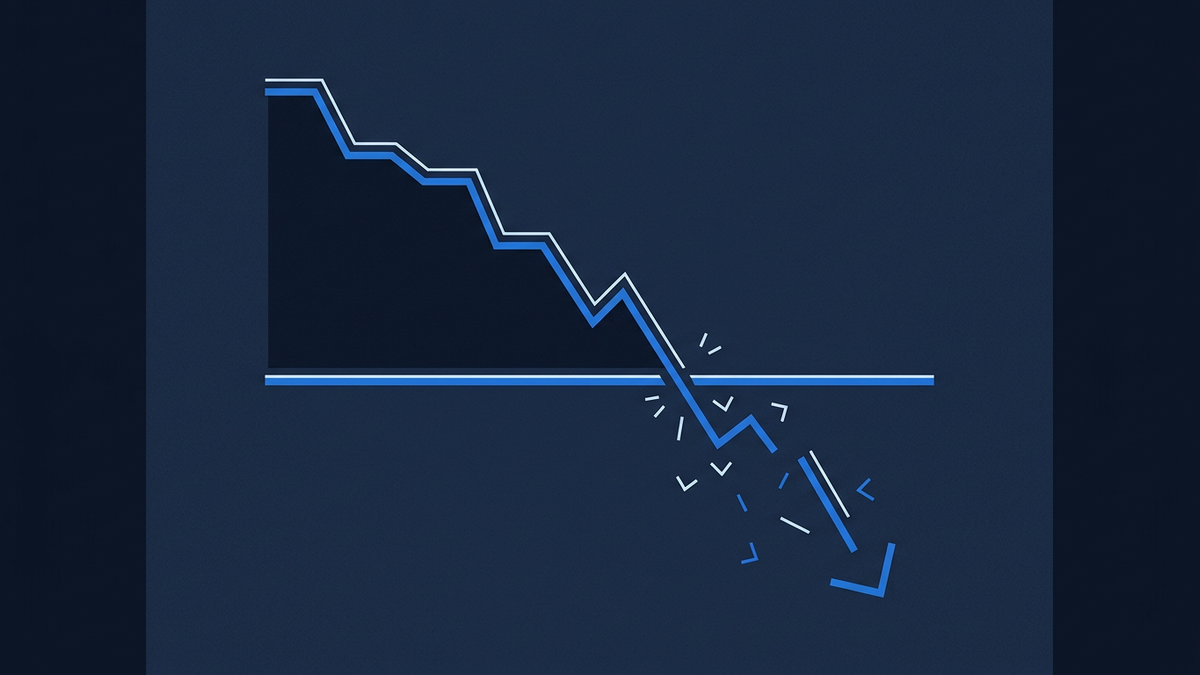

Somewhere on a Bloomberg terminal late on a Wednesday afternoon, a number flashed that crypto traders had been quietly dreading. Strategy, the corporate vehicle that has spent five years buying bitcoin with anything not nailed down, was selling. The amount was almost nothing: 32 bitcoin, about $2.5 million, roughly 0.0038 percent of its holdings, raised to cover a preferred-stock dividend. It was the company's first sale since 2022. The size was trivial. The signal was not. By the time the wires picked it up, bitcoin was sliding into what the FT called its biggest weekly loss since November 2022, the month FTX imploded and took a generation of retail confidence with it.

That comparison is the part worth sitting with. November 2022 was not a normal drawdown. It was the moment the previous cycle ended. So when the same outlet that watched Sam Bankman-Fried's empire dissolve in real time reaches for that benchmark to describe this week, the read-through to prediction markets is immediate. Traders are not asking whether bitcoin is volatile. They are asking whether the cycle has turned.

Why a Strategy sale matters more than the size of the sale

Strategy has been the marginal buyer of bitcoin for most of this cycle. Michael Saylor's pitch, repeated at every conference and on every podcast that would have him, was that the company would never sell. That was the whole thesis. A permanent bid, funded by convertible debt, sucking supply out of the market at any price. The moment that pitch wobbles, the structure of the market wobbles with it.

This is not the same as a hedge fund trimming a position. It is closer to a central bank announcing it will no longer defend a currency peg. The size of the trade is almost beside the point. What matters is what it implies about every future trade. If Strategy can sell, Strategy might sell again. If Strategy might sell again, the convertible-debt-funded perpetual-bid story does not survive contact with the next leg down.

Probability traders clocked this quickly. On the bitcoin price-range market on Polymarket, the higher buckets, the ones asking whether bitcoin touches $150,000 or $200,000 at any point in 2026, have been bleeding implied probability all week. The lower buckets, the ones that until recently looked like leftover crumbs from a more pessimistic era, have stopped bleeding and found some support. None of this is panic pricing. It is something more interesting. It is a slow, deliberate reassessment of what the right-hand tail of the distribution looks like once the marginal buyer becomes a question mark.

What the order flow says versus what the headlines say

The headline number, the worst week since November 2022, will do most of the emotional work this weekend. But the more useful signal sits in the shape of the move. Bitcoin has not crashed in a single afternoon. It has ground lower across multiple sessions on rising volume, with each attempted bounce sold into. That is the texture of distribution, not capitulation. It is what markets look like when the people who were long start trying to get smaller without admitting it.

Polymarket's implied probabilities on the upper price buckets reflect that texture. The decay is gradual, not violent. Traders are not pricing a 2022-style crater. They are pricing something more like a regime change, where the right number for end-of-year bitcoin is meaningfully lower than the consensus that prevailed in April.

And this is the part that separates prediction markets from spot price action. Spot tells you where the last trade happened. A probability contract tells you what a margin-paying trader is willing to bet about the future, knowing that being wrong costs real money. That distinction matters most exactly in weeks like this one, when the narrative is loudest and the actual distribution of outcomes is being repriced underneath. Our explainer on how prediction market odds work covers the mechanics in more depth.

The macro overlay nobody wants to discuss

There is a second story under the Strategy story, and it is the one crypto-native commentators are doing their best to ignore. Bitcoin has spent two years trading more like a high-beta tech proxy than a digital gold hedge. When the Nasdaq sneezes, bitcoin catches whatever the Nasdaq is carrying. The week that the FT is flagging as the worst since November 2022 has not happened in a vacuum. It has happened against a backdrop of rate-path uncertainty and a broader risk-asset wobble.

That overlay shows up in adjacent contracts too. The Fed-path markets have been twitchy for weeks. Traders who watch both books at once have noticed the correlation tightening, not loosening, which is the opposite of what the digital-gold thesis would predict.

The honest read is that bitcoin is being repriced for a world where the corporate-treasury bid is no longer reliable and the macro backdrop is no longer cooperative. That is not the end of the cycle. But it is not nothing either.

So what now

The useful thing about prediction markets in a week like this is that they force a number out of the noise. You can hold any view you like about Strategy, Saylor, the cycle, or the macro overlay. The contract still needs a price. Watching where that price settles, particularly in the lower and upper buckets of the 2026 price-range market, gives you something cleaner than sentiment surveys and something faster than analyst notes. iPredicta tracks bitcoin price-range contracts across Polymarket alongside the regulated US venues, and this week is exactly the kind of repricing the platform was built to surface in close to real time.

Frequently asked questions

Why does a Strategy sale matter so much to the bitcoin price?

Strategy has been the most visible corporate buyer of bitcoin for years, with a stated policy of never selling. Any sale, regardless of size, undermines that thesis and forces traders to reprice the assumption that there is a permanent, debt-funded bid sitting under the market. The signal matters more than the volume.

What are prediction markets actually pricing about bitcoin right now?

The upper buckets on Polymarket's 2026 price-range contracts have been losing implied probability through the week, while the lower buckets have found some support. That pattern is consistent with a regime-change repricing rather than a panic. Traders are adjusting the shape of the distribution, not abandoning the asset.