Pricing happens after the close tonight. By tomorrow lunchtime, give or take a delay, SpaceX is supposed to be a publicly traded stock on Nasdaq under SPCX, having raised roughly $75 billion at a target valuation around $1.75 trillion. That would make it the biggest IPO in history by a comfortable margin, leapfrogging Saudi Aramco's 2019 listing by more than two to one.

And the prediction markets are already saying SpaceX is underpricing itself.

On Polymarket, the SpaceX closing market cap market puts the odds of a first-day close above $2 trillion at 64 percent. The odds of closing above the $1.75 trillion offer valuation sit higher still. The market is not asking whether SpaceX pops. It is asking how big the pop is.

What the deepest contract is actually pricing

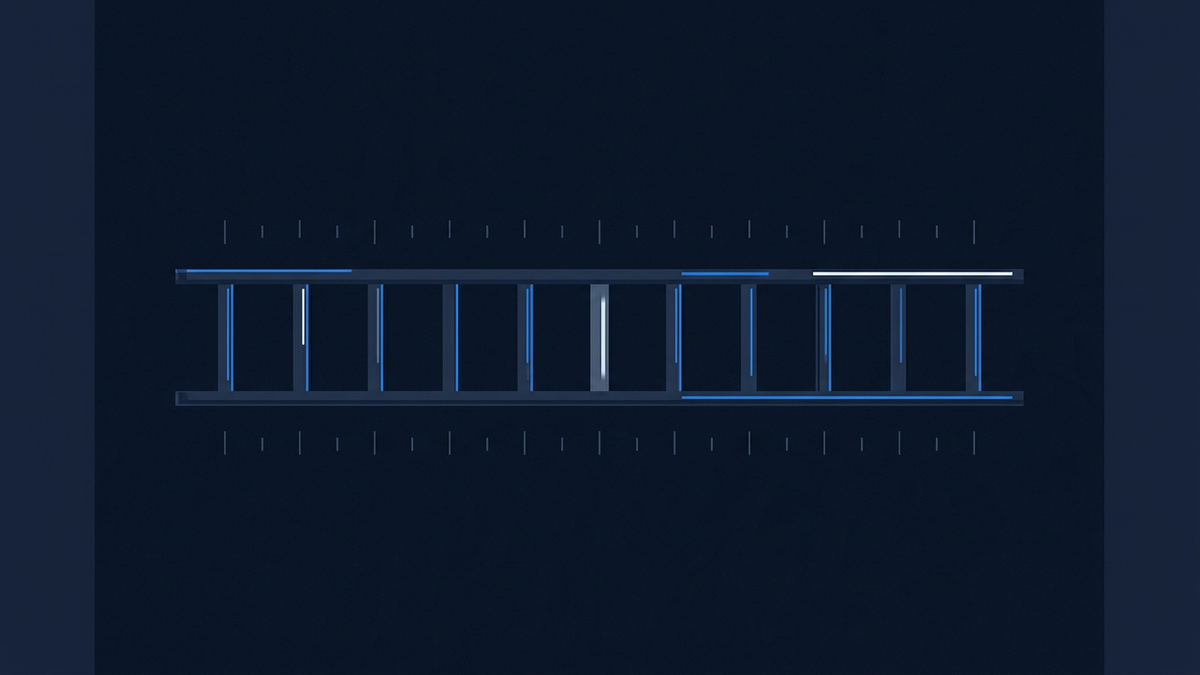

The headline contract, with about $10 million in volume behind it, is a ladder. Each rung asks whether the closing market cap on debut clears a given threshold. The picture it paints is unusually one-sided.

Above $1 trillion: 99 percent. Above $1.4 trillion: 97 percent. Above $1.6 trillion: 92 percent. Above the $1.8 trillion line, which sits just above the S-1 valuation, the market still gives an 85 percent chance, up roughly four points in the last 24 hours. The $2 trillion rung is at 64 percent, up three. The $2.2 trillion rung re-rated harder, climbing six points in a day to 42 percent. Only when you reach $2.4 trillion does the probability drop into clear long-shot territory, at 25 percent.

That is a market saying: the base case is that SpaceX prices at one number tonight and closes meaningfully above it tomorrow. A separate, lower-volume bracketed contract makes the same point in cleaner form. Its modal outcome, at 64 percent, is a close at $2 trillion or above. The bracket containing the actual offer valuation, $1.6 to $1.8 trillion, sits at just 8 percent.

For a primer on how these probabilities are derived from contract prices, see how prediction market odds work.

The share-price market is thin, and worth flagging

There is a parallel contract on the first-day closing share price, and it deserves a health warning. Only about $19 thousand has traded through it. That is a weak signal compared to the cap ladder.

For what it is worth, the modal bracket on that contract is $150 to $200, at 61 percent, up eleven points over the last day. The $135 IPO price sits in the bracket below, $100 to $150, at 30 percent. So even the thin market leans toward a first-day gain over the offer. Just do not read too much into a contract with that little money behind it. Liquidity is the difference between a market that aggregates information and a market that aggregates two traders' opinions, and our explainer on why liquidity matters in prediction markets walks through the mechanics.

The timing and ticker contracts, by contrast, are essentially settled. The June listing month sits at 99.8 percent. The 12 June date sits at 97 percent, with the remaining 3 percent scattered across later dates in the month, consistent with the advisers' own caveat that pricing could slip on market conditions. SPCX as the ticker is priced at 99.9 percent; the joke alternatives never got going.

What could be wrong with all this

The straightforward reading is that institutional demand on the roadshow has been strong enough that the deal is leaving money on the table, and Polymarket traders are calling it.

But a record valuation that the market expects to pop further is also exactly the setup short-sellers and bubble critics have been flagging. A $1.75 trillion offer valuation is already an extraordinary number for any single company. A close above $2 trillion, which the market treats as the modal outcome, would make SpaceX comparable in market cap to the largest listed companies in the world on day one. The scepticism that valuation faces post-debut is the same scepticism it faces pre-debut; the IPO does not resolve it, it just gives the bears something liquid to trade against.

There is also the roughly 3 percent slip probability on the date contract. Not large, but not zero. Advisers themselves have left the door open to a pricing delay if conditions deteriorate between now and the close.

What to watch tonight and tomorrow

Two moments matter. First, the pricing print after the US close on 11 June: where in the range does the book actually clear, and does it come above the $135 target. Second, the opening auction and first-day close on Nasdaq on 12 June, which is the figure the deepest Polymarket contract resolves against.

If the closing cap lands in the $1.8 to $2 trillion zone, the market called the direction but not the magnitude. If it punches through $2 trillion, the modal Polymarket trader was right, and the bracket above $2.2 trillion, currently at 42 percent and rising, becomes the contract to watch in the final hours of trading. If it closes at or below the offer valuation, the ladder gets violently re-rated downward in real time, and the bear case gets its first piece of hard evidence.

None of this is a recommendation to buy or avoid the stock. It is a read of what the smartest available aggregator of pre-debut sentiment is currently saying. iPredicta tracks these contracts across Polymarket and the regulated US venues, and the SPCX cap ladder is sitting near the top of the watch list precisely because pricing day is the moment that ladder either pays out or breaks.

Frequently asked questions

Why does Polymarket think SpaceX will close above its own IPO price?

Strong roadshow demand and tight allocation often produce first-day gains, and traders appear to be pricing that pattern in at scale. The 64 percent odds on a close above $2 trillion, against a $1.75 trillion offer, imply the book is oversubscribed enough that retail buying tomorrow pushes the price higher. It is a directional read, not a guarantee, and the brackets above $2.4 trillion show traders do not expect the move to run forever.

How does the closing market cap contract actually resolve?

It resolves based on the official closing price of SPCX on its first trading day on Nasdaq, multiplied by total outstanding shares, as reported on the primary exchange's listing page. If no IPO happens before the end of 2027, all the cap rungs resolve No. The thresholds are unambiguous numbers, which is why the contract is one of the cleaner ladder markets currently live.