The interesting thing about a retirement announcement from a member of Congress is not the announcement itself. It is the cluster. One member says they are leaving, and within a fortnight three more letters land. Then another five. The shape of that cluster, more than any single name on it, is what tells you something real about the party's read of its own footing going into a midterm.

That shape is exactly what one Polymarket contract is trying to put a number on. The market asks, in plain English, how many Republican House members will not run for reelection in 2026, and slices the answer into a series of count bands. As of 17 June, the Republican retirement count market on Polymarket has one band carrying most of the weight, with a non-trivial tail in the highest count bracket.

What the bands are actually saying

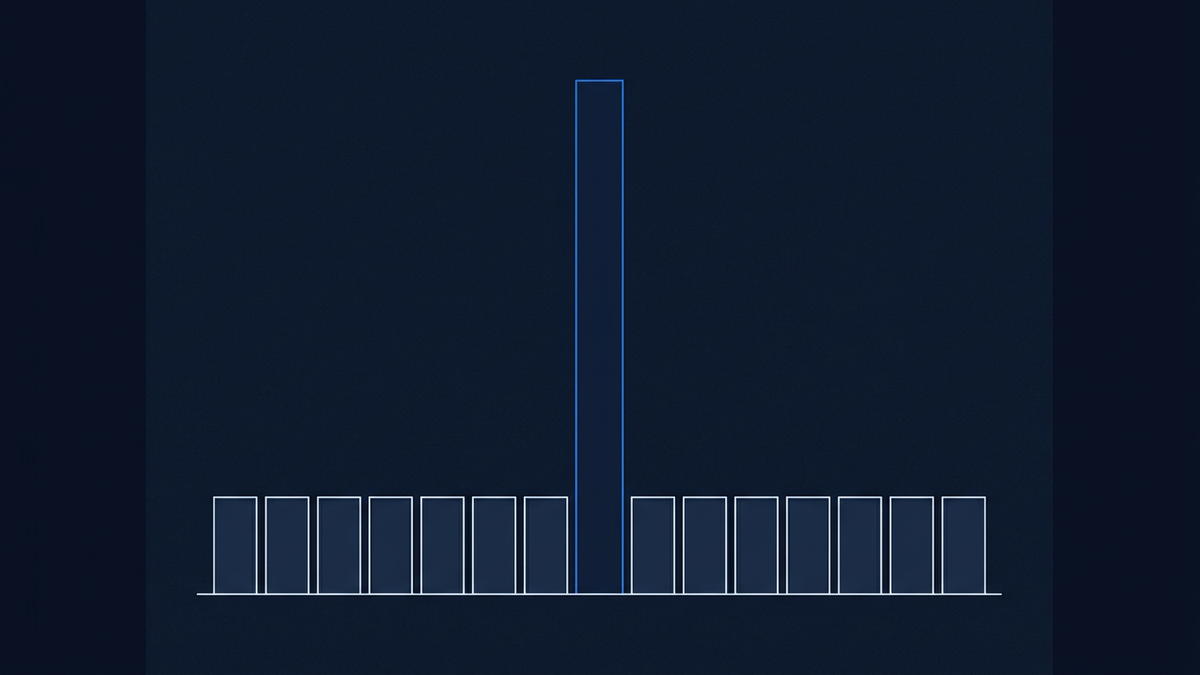

The 36 to 39 band is where the bulk of the conviction sits, trading around 59% as of 17 June. That is the kind of level that says traders have a working central estimate and are happy to defend it. Nothing dramatic, no scramble, no breakdown. Just a band that has accumulated weight as the announcements have piled up through the spring.

The other notable feature is further out. The 44-plus rung sits around 16% as of 17 June 2026. That is not a marginal corner of the contract: roughly one in six is a meaningful tail. It does not say a wave is coming. It says the high-count outcome is priced as a live possibility rather than dismissed outright.

Under the central band, the lower count outcomes are where the air gets thin. The 24 to 27 and 32 to 35 bands each sit in single digits, and the deep-low 28 to 31 band is barely registering at 2%. The market is, in effect, saying: it will probably be a normal-ish retirement cycle by recent standards, but if it surprises, it surprises in the direction of more departures, not fewer.

Why count-band markets are useful, and where they are not

A contract like this is doing something polls and pundit columns cannot easily do. It is forcing a distribution. Anyone who has read a thumbsuck retirement preview in the past six months will have seen the same hedged sentences about how "some analysts expect a larger-than-usual class". The market makes those analysts pick a band and put money on it.

That is the appeal of a count-band market over a single yes-or-no contract: you get a probability distribution instead of a binary, and you can read where the weight sits, where the tail is, and how much disagreement there is between adjacent rungs. The 44-plus level being non-trivial while 28 to 31 is essentially flat tells you something the central band on its own does not.

The limit of a contract like this is also worth flagging. The resolution date is set by the calendar, not by the news. There are still months in which a member can quietly file paperwork, lose a primary, accept an administration job, or decide to run for governor. Each of those routes counts toward the same denominator, but they are very different political signals. The market does not distinguish between a member retiring because they are tired and one running for a Senate seat because they smell opportunity. It just counts them.

What the tail actually buys you

A non-trivial probability on 44-plus is the part of this market doing the most analytical work right now. It is the rung that says: maybe the central estimate is too tidy. Maybe the cluster is not done.

This is why reading the full distribution matters more than fixating on the favourite. A 59% headline number on the central band sounds like a settled view. The 16% on the upper tail, sitting next to it, complicates that read. Traders are paying real money for the optionality that the count goes high, which is a different proposition from saying they expect it to.

This is also where these contracts contrast usefully with the political-polling apparatus. A poll might tell you that voters are unhappy with the majority party, or that the generic ballot has narrowed. It is much harder to translate that mood into a single number for retirements. A market does the translation for you, badly perhaps, but visibly. You can see what traders think the mood is worth in headcount.

The structural question this market poses

Strip away the bands and the percentages, and the question this contract is really asking is whether the 2026 cycle will look unusual. A central band that sits in the high thirties is, broadly, the kind of number that says nothing exceptional is happening. A tail that is willing to pay for 44-plus is the part of the market hedging against the possibility that something is.

That tension, between a confident central estimate and a live upper tail, is the structural feature worth watching. It is also why the contract does not need urgent news flow to be interesting. The next retirement letter will move it. So will the absence of one. iPredicta tracks contracts like this Republican retirement count alongside the rest of the 2026 US politics shelf, because the slow accumulation in a market like this often tells you more than the day's headlines.

Frequently asked questions

What counts as "not running" for the purposes of this market?

Per the contract terms, a member counts if they publicly announce retirement from Congress, choose to run for a different elected office in 2026 instead of their current seat, or otherwise do not seek reelection to that seat. It is a wide net by design, and it does not distinguish between someone leaving politics entirely and someone trying to move up to a Senate or gubernatorial race.

Why does a count-band market matter more than a single retirement headline?

A single announcement is a data point. A count band forces traders to express a view on the full distribution, which is where the political signal lives. The shape of where the weight sits, and where the tail goes, tells you how the people putting money down are reading the cycle as a whole, not just one resignation.