A Kalshi contract on whether the 49ers beat the Packers looks, at first glance, identical to a FanDuel bet on the same game. Both pay out if your pick wins. Both display odds or prices that reflect how likely the market thinks each outcome is. Both let you lock in a position and settle when the game ends. The user experience has converged to the point where it is legitimately hard to tell them apart without looking closely at the footer.

They are, however, different products in meaningful ways, different enough that US law treats them as belonging to different regulatory agencies, different enough that your tax treatment differs, different enough that the consumer protections you have access to when something goes wrong differ. For the heavy majority of users placing a few trades a month on a game they care about, those differences do not matter. For the smaller but growing population of serious traders, they matter a lot.

This guide covers the mechanical differences, the legal differences, the tax treatment, and who each product actually suits. It applies primarily to the US market, where both prediction markets and sports betting are legal and widely available. The UK has its own parallel framework, UK betting exchanges have offered peer-to-peer contracts since 2000, and the distinctions work differently under UK law. For our UK readers, the relevant equivalent is our guide to whether prediction markets are legal in the UK.

This is an educational overview, not legal, tax, or financial advice. If the tax treatment or legal framework is material to a decision you are making, consult a professional who knows your specific situation.

The mechanical difference

A sportsbook is a bookmaker. You bet against the house. The sportsbook sets the odds, accepts your wager, and holds the other side of the bet itself. If you win, the sportsbook pays you. If you lose, the sportsbook keeps your stake. The sportsbook's profit comes from the vig, the margin built into the odds, which means the sum of the implied probabilities on both sides of a bet is always greater than 100%. At typical vig of 4.5%, betting $100 on each side of an evenly-matched game loses you $4.50 regardless of outcome. This is the house edge.

A prediction market is an exchange. You do not bet against the house, you buy or sell contracts against other users. The market price is set by order flow: if more people want to buy Yes than sell Yes, the price goes up. The platform itself takes no position on the outcome. Its revenue comes from transparent per-trade fees, typically much smaller than a sportsbook's vig and paid only on the trades you actually make.

The economic consequence of this difference is meaningful over time. A sportsbook's vig of 4 to 5% is a compounding tax on every bet. A prediction market's fees, typically well under 1% per trade, and only on the taking side, represent far less drag. For a user placing thousands of dollars a month in bets, the cost difference between the two structures can run into hundreds of dollars a year on identical trading activity.

The other mechanical difference is early exit. Sportsbooks historically did not let you close a position before the event, your stake was locked in. Modern sportsbooks offer "cash out" at terms favourable to the operator, which is not quite the same thing. On a prediction market, you can sell your contract any time there is liquidity in the order book, at whatever the market price is right now. If your Yes contract has moved from 40¢ to 65¢ because of new information, you can take that 25¢ profit immediately rather than waiting for resolution.

Pricing transparency

Sportsbook odds are set by the operator. They are based on a combination of statistical models, market-maker data, and, critically, the operator's exposure. If the sportsbook has taken too much action on one side of a bet, it will move the odds to balance its book, even if that means the odds no longer reflect true probabilities. This is not a flaw in the model; it is the model. A sportsbook's job is to balance its exposure, not to produce accurate probabilities.

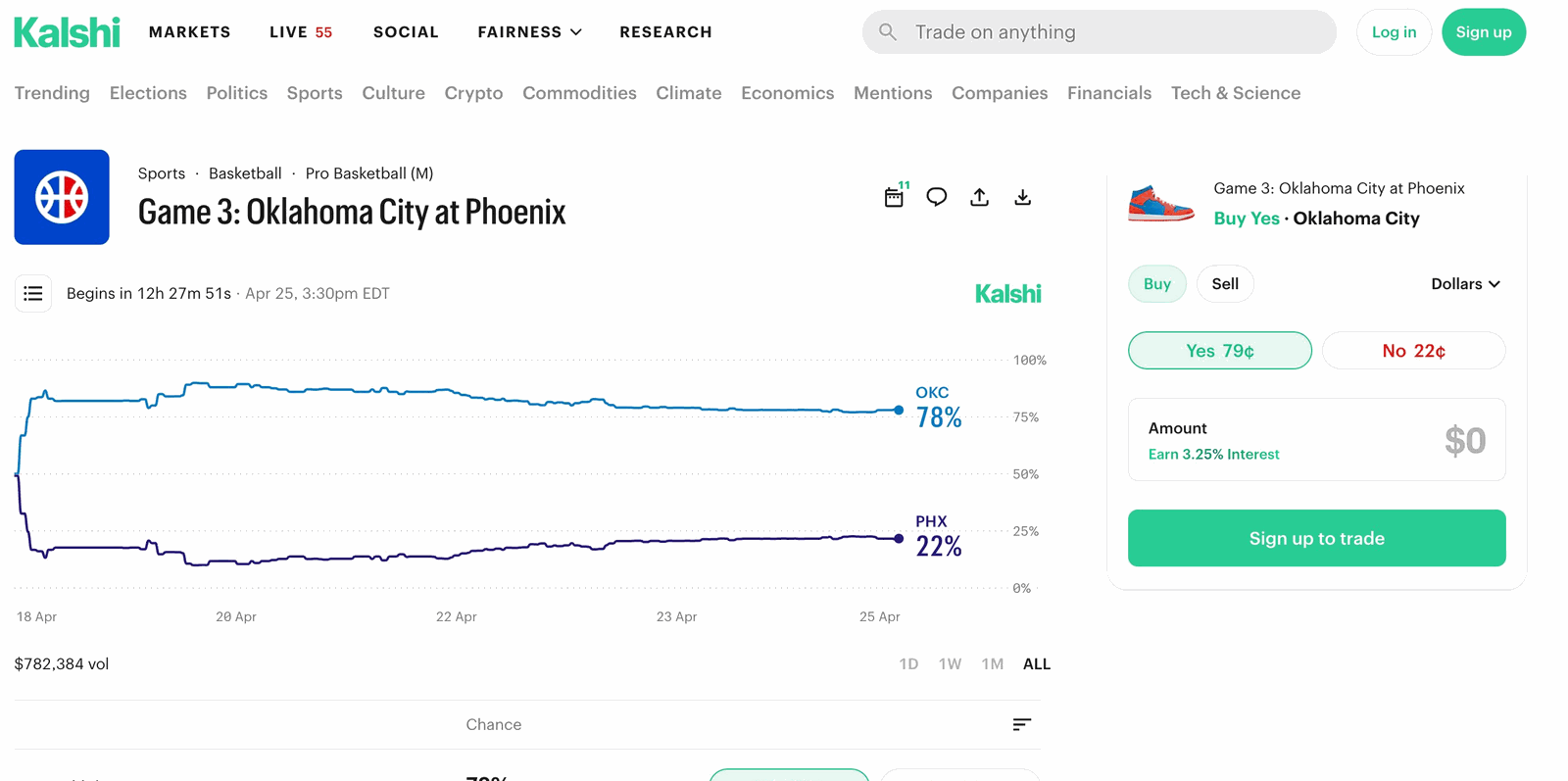

Prediction-market prices are set by trading. They reflect the collective view of everyone willing to take a position, weighted by how much they are willing to stake. The platform has no exposure and therefore no incentive to push prices away from consensus. Research on prediction-market accuracy consistently finds that in liquid markets, prediction-market probabilities outperform both expert forecasts and statistical models. Sportsbook odds do not have this property, they are not designed to.

The practical implication: if you want the most accurate available probability on a given event, prediction-market prices are the better source. If you want a bet that you cannot close early and that pays out at fixed odds, a sportsbook is the simpler product. Both have their uses. For more background on how prediction markets generate their probabilities, see our guide to what prediction markets are.

Regulation

In the US, sportsbooks and prediction markets are regulated by different authorities under different laws, and this is the difference that has produced all the current litigation.

Sportsbooks operate under state gambling laws. Each state sets its own licensing regime, regulatory body (usually a state gaming commission), allowed products, tax rates, and consumer protections. Thirty-eight states plus DC have legal sports betting as of April 2026. The products available in California, Texas, or Oklahoma are materially different from those in New York or New Jersey, because the state frameworks are materially different.

Prediction markets operate under federal commodities law. Kalshi and Polymarket US are designated contract markets under the CFTC, which governs derivatives exchanges. The theory, contested by several state regulators, is that this federal status preempts state gambling law. That contest is the central legal question in the US prediction-markets industry right now and is heading toward the Supreme Court. For the full state-by-state picture, see our guide to whether prediction markets are legal in the US.

The practical consequence for users: sports betting is available in specific states and not others. Prediction markets are federally approved in all 50 states, with state-level access constrained where active litigation has produced court orders restricting specific platforms in specific states. In states without legal sports betting, Kalshi has offered a route to trade on sporting outcomes, which is precisely why state-level pushback has been so aggressive in some jurisdictions.

Tax treatment

US tax treatment for sportsbook winnings and prediction-market winnings differs, though the difference is often glossed over in the coverage.

Sportsbook winnings are treated as gambling income under IRC section 165(d). You report winnings on Form 1040 Schedule 1 as other income. You can deduct losses up to the amount of your winnings, but only if you itemise deductions, which fewer taxpayers do since the 2017 Tax Cuts and Jobs Act raised the standard deduction. For most recreational sports bettors, this means winnings are taxed in full and losses are not deductible. Withholding applies on winnings above certain thresholds.

Prediction-market winnings are treated differently. Kalshi contracts, as CFTC-regulated swaps, are subject to section 1256 contract treatment in some interpretations, which means 60% long-term capital gains and 40% short-term capital gains regardless of how long you hold. This is materially more favourable than ordinary income treatment. Polymarket US's tax treatment is less settled because the platform is newer and the IRS has not issued guidance specific to its structure. Consult an accountant, prediction-market tax is genuinely complicated and worth getting right if you trade above nominal amounts.

The tax advantage for prediction markets is one of the quieter but most significant differences versus sportsbooks for frequent traders. Over a year of active trading at meaningful size, the difference between 37% ordinary income tax and blended 60/40 capital gains treatment can amount to thousands of dollars.

Consumer protections

State sports-betting regulation includes substantial consumer-protection requirements: deposit limits, self-exclusion programmes, problem-gambling resources, advertising restrictions, responsible-gambling messaging. These are not incidental, they are the political justification for why sports betting is allowed at all. The state-level regulatory framework treats sports betting as a potentially harmful activity that requires active consumer safeguards.

Prediction-market regulation under the CFTC does not include the same framework. CFTC rules focus on financial instruments and market integrity, preventing manipulation, ensuring fair markets, protecting against fraud. They do not include dedicated problem-gambling protections because the CFTC does not regulate gambling. This is one of the state regulators' core arguments in the preemption litigation: that allowing sports-event contracts on CFTC-regulated platforms effectively creates a parallel sports-betting market without the consumer-protection regime that state gambling laws provide.

For most users this does not matter. For users at risk of problem gambling, it does. The self-exclusion programmes available through state-licensed sportsbooks, which allow you to voluntarily exclude yourself from all licensed operators in a state, do not extend to federally-regulated prediction markets. This is a real gap. If you are someone who needs that kind of safeguard, understand that prediction markets do not currently provide it.

Who each product suits

Sportsbooks are the simpler product. If you want to place a bet on a game, lock in the odds, and find out at the end whether you won or lost, a sportsbook is the more straightforward experience. The products are mature, the UIs are polished, the promotional structures (welcome bonuses, parlay boosts, free bet credits) are familiar. For recreational users placing small-stakes bets on games they watch, sportsbooks are the path of least resistance.

Prediction markets suit users who want better pricing, want to close positions early, care about the tax treatment, or want access to markets outside sports. They also suit users in states without legal sports betting, at least until the preemption question resolves. And for anyone trading at meaningful size, the fee difference versus sportsbook vig is material enough to matter. For a comparison of the two main US prediction-market platforms, see our guide to Polymarket vs Kalshi.

The two products will probably coexist for the foreseeable future, with some convergence in UX and some continuing divergence in structure. The deeper question, whether sports-event contracts on federally-regulated platforms should be allowed at all, is one for the courts and Congress to settle, and their answer will shape the category for the next decade.

How iPredicta fits in

iPredicta covers prediction markets across all categories, sports, politics, economics, entertainment, crypto. We do not aggregate sportsbooks because the products are structurally different and most users approach them for different reasons. What we do is make it straightforward to see prediction-market prices on the events you care about, compare them against the implied probabilities sportsbooks are offering, and identify when one product is materially better-priced than the other.

For users trying to understand which product fits their situation, we are also building a jurisdiction-aware availability layer: enter your state, see which prediction markets are available to you and under what restrictions. That infrastructure matters in a category where availability changes on a court's timetable.

Frequently asked questions

Are prediction markets the same as sports betting?

They look similar but operate on fundamentally different mechanisms. A sportsbook is a bookmaker that sets odds and takes the other side of your bet, profiting from the vig built into the odds. A prediction market is a peer-to-peer exchange that matches you against another user who believes the opposite, profiting from a small per-trade fee. The legal, tax, and consumer-protection consequences differ materially. In the US, sportsbooks are state-regulated under gambling laws while prediction markets are federally regulated under the Commodity Exchange Act.

Is Kalshi a sportsbook?

No. Kalshi is a federally-regulated derivatives exchange under CFTC oversight, not a state-licensed sportsbook. The distinction is mechanical and legal. Mechanically, Kalshi matches users against other users on yes/no event contracts; a sportsbook sets the odds itself and takes the opposite position. Legally, Kalshi operates under the Commodity Exchange Act rather than state gambling laws, which is precisely the point at issue in the ongoing state-level litigation. State regulators argue Kalshi is offering sports betting in everything but name; Kalshi argues federal commodities law preempts that view.

Do prediction markets pay better than sportsbooks?

For equivalent outcomes, prediction markets typically offer better effective pricing because they have no vig built into the odds. Sportsbooks bake a 4 to 5% margin into their lines, which means the implied probabilities sum to more than 100% and the operator profits regardless of outcome. Prediction markets charge a transparent per-trade fee, usually well under 1%, paid only on the trades you actually make. For frequent traders the cumulative cost difference can run into hundreds or thousands of dollars per year on identical trading activity.

How are prediction-market winnings taxed?

US tax treatment is genuinely complicated and depends on the platform and contract structure. Kalshi contracts, as CFTC-regulated swaps, may qualify for IRC section 1256 treatment, 60% long-term capital gains and 40% short-term capital gains regardless of holding period, which is materially more favourable than the ordinary income or gambling income treatment that applies to sportsbook winnings. Polymarket US tax treatment is less settled because the platform is newer. For active traders, the tax difference versus sportsbooks can be significant. Consult an accountant who specifically understands prediction-market structures.

Can I use prediction markets in states without sports betting?

Yes in most states, though access depends on current litigation. Federally-regulated prediction markets like Kalshi are available in around 44 states regardless of whether the state has legal sports betting. The federal preemption question is unresolved and heading toward the Supreme Court. For now, users in states without legal sports betting can typically access Kalshi for sports event contracts, subject to whatever state-level restrictions are active in their specific jurisdiction, always check Kalshi's current state-availability page before signing up.